This too shall pass…

Encasa Financials’ Canadian Equity Fund sub-adviser, Genus Capital Management, and Canadian Short-Term Bond Fund and Canadian Bond Fund sub-adviser, Addenda Capital, recently assessed the impact of Coronavirus on global markets and economies.

Overall, Genus is optimistic on the medium-term impact of the virus on markets, viewing last week’s declines as a healthy correction in what has been a prolonged bull market. Addenda anticipates a V-shaped recovery where we see a sharp decline in markets followed by a sharp rise back to their previous peak. Both sub-advisers also note that the virus is disrupting global supply chains and hurting demand and consumption, which will have a negative effect on global economies in 2020. However, markets experiencing corrections and volatility as we are currently experiencing have a tendency to return to their previous highs within three to four months.

Learn more about the impact of the Coronavirus on global markets by reading Addenda Capitals’ report below and reading Assessing the impact of coronavirus on the markets: Our view by Genus Capital Management.

The Impact of the COVID-19 Epidemic on the Economy and Markets, Addenda Capital

Benoît Durocher: Executive Vice President and Chief Economic Strategist

Yanick Desnoyers: Vice President and Senior Economist

The COVID-19 epidemic is raising fears of an economic slowdown, even of a recession. As of early March however,economic momentum seems to generally be strong enough to withstand the bug’s negative impacts. In a nutshell, the virus’s effects are akin to a supply shock on the economy, as opposed to a demand shock. Supply chains are hampered as many Chinese suppliers have shut down production; transportation services are curtailed and businesses are considering, or are implementing, travel restrictions. Data as of this date have not yet reflected that these measures have taken their toll on output and employment, the latter being a sign that the supply shock would be turning into a demand shock.

Qualifying further, there will likely be a dead weight loss to Chinese GDP, and therefore to global GDP, for the first quarter. The degree of propagation to other economies will depend on the degree of openness to virus infected countries, particularly China. (Another significant epidemic centre is Iran which isn’t as integrated in global supply chains; Italy and South Korea are more so). On that basis, the economy of Germany is at risk while that of the United States is relatively shielded given that total goods imports account for close to 15% of GDP. Not insignificant, but nowhere near household spending’s close to 70% share.

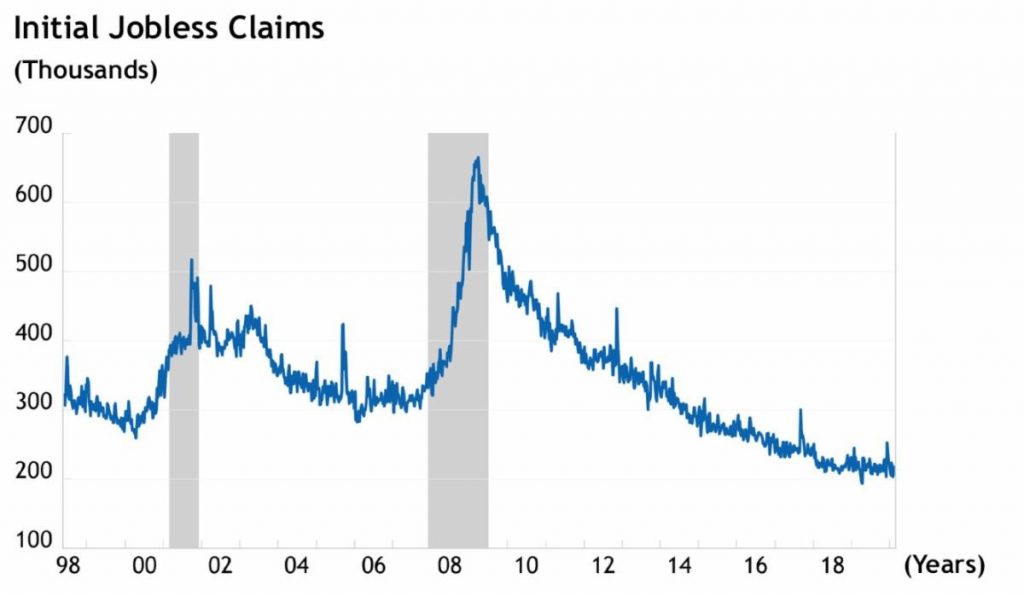

To gauge if the supply shock is morphing into a demand shock which could therefore impact household spending, we are keeping a close eye on labour market indicators. Aside from the monthly non-farm payrolls and labour force surveys, which for January were not showing signs of weakness, there is weekly unemployment insurance claims data released every Thursday. Released on February 27th, initial claims (see chart), still hadn’t revealed contamination from the virus to the US labour market.

Source: Refinitiv

Still, there could be a change to this situation should the US labour market be hit. This could result from US firms being cut off from inputs from overseas. As stated, we are monitoring this closely, but our base case still remains that there will be a V-shaped reaction once the epidemic eases. We will rely on credible scientific data to assess the epidemic’s evolution.

Financial markets are interpreting the information differently though. To be sure, one could argue that the more-than-fairly-valued equity markets are assuming a close to worst case scenario. Equity markets, given their high valuations, seemed ripe for a correction whatever the trigger. The correction led to investors seeking shelter into the perceived safety of government bonds; corporate and provincial credit spreads increased.

In spite of recent much easier financial conditions resulting from the decline in bond yields and the drop in oil prices, market participants still seem to be looking to central banks to step in even if central bank tools are designed to address cyclical, i.e. demand shocks, rather than supply-side shocks. Sure enough, the US Federal Reserve answered the markets’ call by lowering its Fed Funds target range by 50 basis points on March 3rd, soon after G7 finance ministers and central bankers had issued a non-committal statement that they would be intervening to cushion the blow from the virus. The Fed moved a few weeks ahead of its regularly scheduled meeting in an effort to soothe markets’ fears. Equity markets seemed to demand more from the central bank as major US stock indices closed lower by around 3%. (Markets seemed to reassess their reaction at the open of the March 4th session as they were up more than 1% in early trading.)

Turning back to the real economy, US personal income data released for January, though somewhat dated, show that consumers’ purchasing power is expanding. In addition, the report provided more insight on inflation as the price index for personal consumption expenditures, the Fed’s inflation target measure, inched up to 1.7%, getting closer to its 2% target. Consumer price inflation for January in the United States runs at 2.5% while it stands 2.4% in Canada. The Bank of Canada disregarded the overshoot of its inflation target and chose to follow the Fed down the path of lower rates by lowering the bank rate by 50 points today. Hopefully, these measures will prove enough to eradicate the virus and its economic impact.